Loopholes for Some, Taxes for Everyone Else

PDF: Steinberg, Loopholes for Some

Add the word “taxes” to the title of an article or conference paper, and you’re guaranteed to attract an enthusiastic group of artists and art historians. Just kidding. A few like-minded policy wonks might stick around, but generally, terms like hobby-loss rule, offshore incorporation, and limited-liability company are received with confusion and frustrated boredom. But that’s precisely the point! Behemoth companies, such as Nike and FedEx, have lobbied and lawyered up for decades to keep tax avoidance schemes plentiful. Responding to the largely invisible power of tax law, artists such as Lowell Darling and the duo Paolo Woods and Gabriele Galimberti have become artist-investigators—realizing work directly shaped by and from tax law, and in so doing, demonstrating and antagonizing the invisible power that “boring” policy wields both within and beyond the borders of the United States.

Under the so-called hobby-loss rule, the proposed federal income tax deductions of cash-strapped artists and musicians can be disallowed if practitioners do not display a “profit intent.” In the spring of 1969, when Darling filed his federal income tax return for the previous year, the Internal Revenue Service (IRS) disallowed his proposed $870 deduction for the cost of art materials under the justification that Darling was a hobbyist rather than an artist demonstrating a profit intent. On its face, the hobby-loss rule is aimed at curtailing attempts by taxpayers to offset expenses incurred from hobby-like activities against their principal source of income—such as a medical doctor claiming also to be a tennis player and taking deductions for equipment and club membership fees.1 Darling’s response to his classification as a hobbyist articulates how such regulations play out in practice: “What is or isn’t an artist shouldn’t be dependent on the sale of things.”2

Situating tax law as the foundation for the next decade of his art, Darling engaged in a paradoxical practice: demonstrating a profit intent by publicizing and trading his work while keeping his balance sheet at a steady zero. As a full-time artist with a Master in Fine Arts (MFA) from Southern Illinois University, Darling established the fictional Fat City School of Finds Art, issuing free MFA and PhD diplomas at “Congraduating” events. He published Notes from Fat City: Artist’s Proof (1970), a limited-edition folio documenting his pro bono practice—an “exclusive” item that he donated to various art-collecting institutions and individuals. The folio even includes reproductions (stamped with “Artist’s Proof”) of ludicrous correspondence between himself and government representatives and institutions that document and discuss his art practice.3

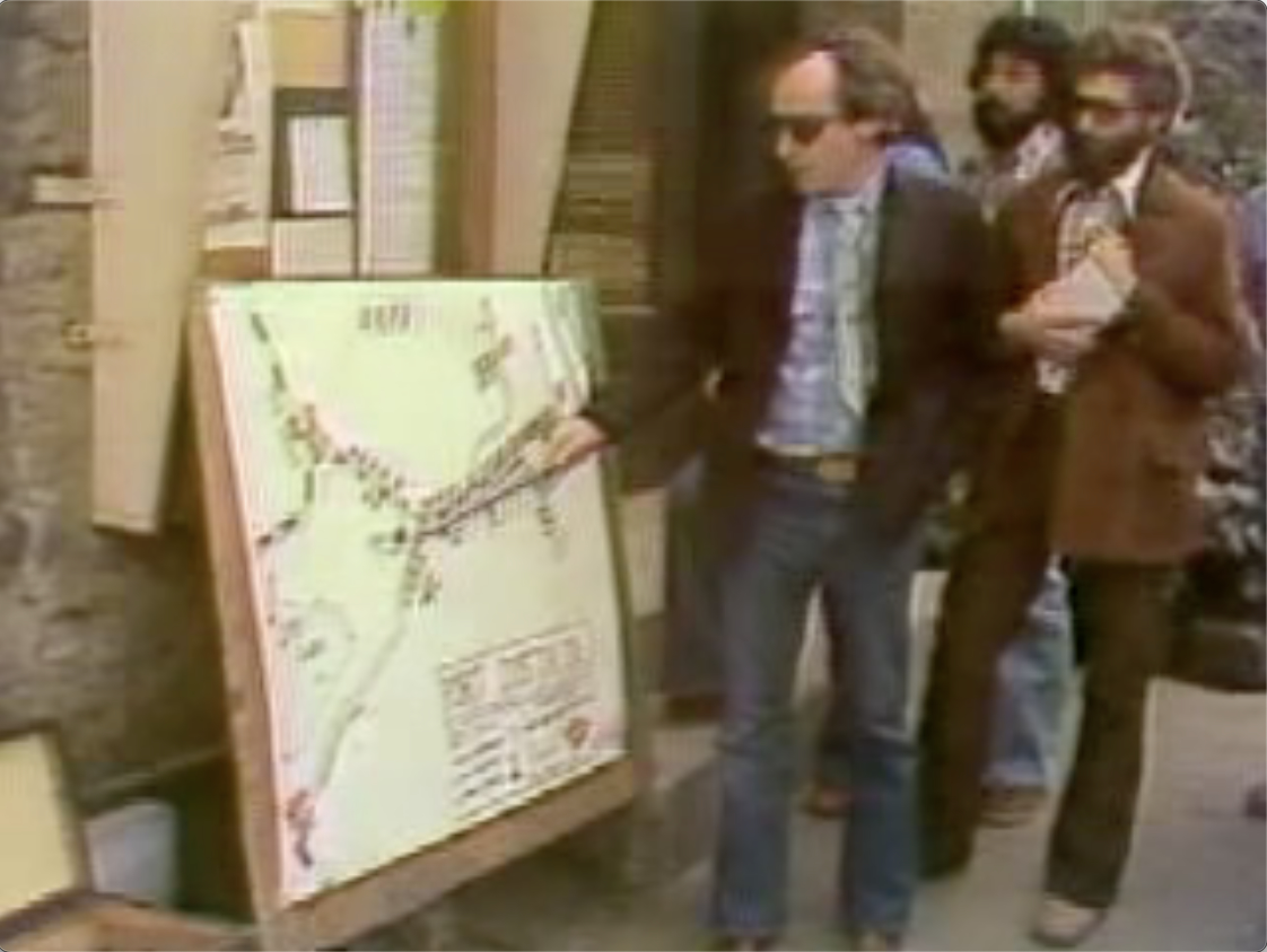

Darling also realized public(ized) artworks of “urban acupuncture” beginning in the late 1960s. In 1975, to cure Los Angeles’s economic and environmental woes, Darling acupunctured the city by placing needles into the ground at several locations. Elisabeth Coleman (who later became Governor Jerry Brown’s press secretary) reported on the performance in a four-minute segment on Los Angeles’s Channel 7 (ABC) Eyewitness News. The project received such attention that Los Angeles Mayor Tom Bradley personally thanked Darling for his “symbolic acupuncture.”4 In 1977, when the three-hundred-resident town of Port Costa, California, was facing a $10,000-a-day fine for its illegal sewage system, Town Councilman Clayton Bailey requested Darling’s assistance: “I am writing to you Mr. Darling, at the ‘Center of World Problems.’ Your services have been acknowledged by . . . the City of Los Angeles, and the State of California; I understand that you are the world’s leading authority on urban acupuncture.”5 With the exaggerated fanfare of a patent medicine salesman, Darling began his pro bono public art at Port Costa’s post office (fig. 1), explaining that acupuncturing a city is like acupuncturing a body and that locating the problematic area of Port Costa’s “body” was an easy task—simply follow the smell.6

Darling’s performances demanded press coverage not only because he distributed press releases ahead of his arrival but also because of the performances’ entertainment value as news.7 The stunts were grounded in the press’s recognition that such headline-grabbing events would hold readers’ and viewers’ attention. Darling’s career benefited greatly from this earned media, all the while affirming his work as art and his status as an artist. In this way, Darling’s practice was shaped by and for tax law, performing the IRS’s definition of professional activity.

In an elegant example of the cultural value of such paradoxical law-following practices, in 1973, the federally funded National Endowment for the Arts (NEA) awarded Darling a three thousand–dollar grant.8 As Darling summarizes: “One branch of the government was giving me money because I was an artist, another taking it from me because I wasn’t.”9 In 1974, the IRS revised Darling’s tax classification from a hobbyist to an artist displaying profit intent, reimbursing the initial claim of $870 (plus interest); this change in status was not because Darling had demonstrated profit intent but because he had demonstrated profit in the form of the NEA grant.

Artists Paolo Woods and Gabriele Galimberti target a different area of tax avoidance: obtuse financial secrecy mechanisms also known as tax havens. Their work, like Darling’s, is temporal and investigative, unfolding like a true-crime tale infused with layers of intrigue and humor. Of course, the term “tax haven” is a slight misnomer; these “sites” are less about taxes than they are about secrecy; indeed, they are generally rebranded as simply international financial centers. The 2021 Annual Report of the Delaware Division of Corporations boasts, in bold text, that amid the economic struggles of the COVID-19 pandemic, they have “experienced unprecedented growth,” adding over 336,407 business entities in 2021 alone.10 Delaware is one of four states in the United States that has no corporate income tax, and at present, it is “home” to roughly 67 percent of Fortune 500 companies and over half of US-based publicly traded companies. The Tax Justice Network ranks the United States as the world’s second largest tax haven (or secrecy jurisdiction), after the Cayman Islands. So, how might one visualize the operations of furtive and abstract legal entities designed to facilitate obfuscation and veil the wealth and assets of high-net-worth individuals (HNWIs) and corporations? The answer, it seems, is paradoxical and humorous law following.

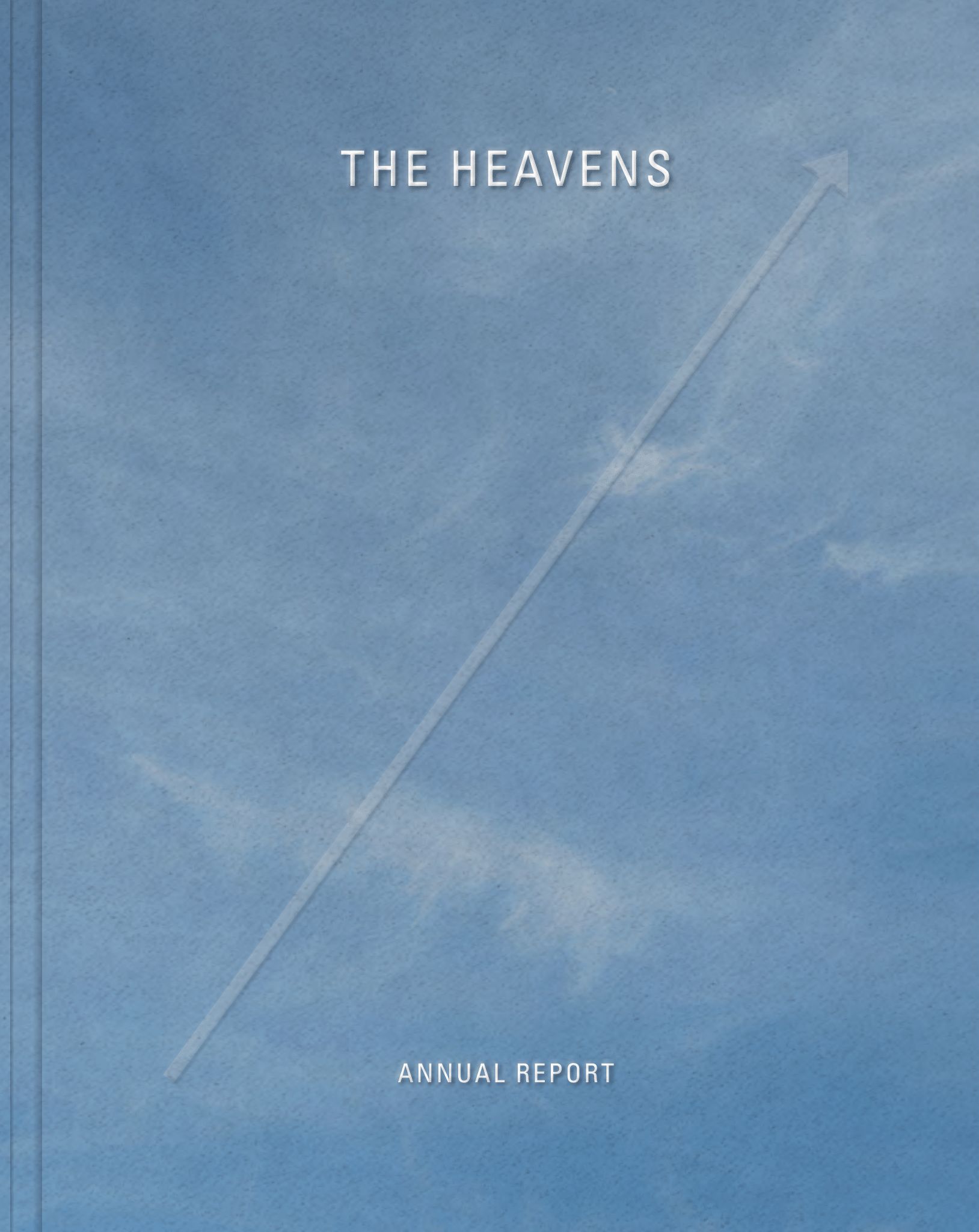

Woods and Galimberti take as their starting point legal tax avoidance, documenting the ease with which they were able to lower their own tax liability. On October 23, 2014, they visited the drab brick office building of the Corporation Trust Center in Wilmington, Delaware, and signed paperwork to incorporate as “The Heavens LLC.” Legally, they moved into an immaterial office space and assembled their invisible cubicle next to Coca-Cola, Wal-Mart, and Alphabet Inc. (namely, Google, which incorporated in Delaware in 2003, one year before their initial public offering [IPO], restructuring in 2015 to become a subsidiary of Alphabet). The artists spent roughly two years traveling the world, photographing a selection of those non-sites that facilitate offshore incorporation. Then, in 2015, they did what any responsible limited-liability company would do. They published, as an artists’ book, The Heavens: Annual Report.11

A blue sky with wispy, feather-like white clouds adorns the publication’s book sleeve and outer covers (fig. 2); the front is accented with a debossed upward-pointing arrow, suggesting financial prosperity. A pie-chart-turned-table-of-contents introduces readers to financial statements and balance sheets of a different sort. The book intermingles an essay by Nicholas Shaxson, a journalist and staff writer for the Tax Justice Network, with luscious photographs that give a sense of place to hopelessly abstract legal entities. Within the pages is a photograph of the residence of the Lord Mayor of the City of London (fig. 3). The City, as it is frequently called, is a small municipality and financial center within the greater London metropolis; it is the lynchpin for an offshore global financial system comprising current and former British colonies. There is also a photograph documenting endless rows of post office boxes on Grand Cayman (in the Cayman Islands) and another showing Perrotin Gallery’s Hong Kong branch, with a caption suggesting that art is a safer investment than stocks. An image of a white room with gray cabinets documents a high-security vault in the Singapore Freeport—a site facilitating the storing, buying, and selling of artwork, which is located within a larger “free zone” that is not subject to normal tax and customs rules. There are even photographs documenting the services and state entities facilitating the artists’ own tax-avoidance maneuvers—specifically, their letter of incorporation and a photograph of the office in which they became The Heavens, the limited-liability corporate entity under which they realized this project about the very mechanisms they were exploiting.

Much like art is the stuff of fabrication, bringing imagination into reality, so too are the standards separating hobbyist from artist and the incorporation schemes that have less to do with residency than with privacy. Shifting bureaucratic classifications and categories can be the difference between a tax liability of millions and zero. In taking tax law as their starting point, these artists demonstrate not only how law shapes art but also how taxes shape the behaviors of individuals and corporations in powerful ways.

Cite this article: Monica Steinberg, “Loopholes for Some, Taxes for Everyone Else,” in “Beyond Copyright: How does Law Impact Art?” Colloquium, ed. Wendy Katz and Lauren van Haaften-Schick, Panorama: Journal of the Association of Historians of American Art 9, no. 1 (Spring 2023), https://doi.org/10.24926/24716839.17434.

Notes

- Darling’s 1968 federal income tax return was subject to the Revenue Act of 1954, 26 U.S. Code § 270. This was replaced with the Tax Reform Act of 1969, 26 §183, applying to income derived after December 31, 1969. The revision had no effect on Darling since his activity was still deemed a hobby (lacking a reasonable expectation of monetary profit). ↵

- Lowell Darling, quoted in Mark Jonathan Harris, “ . . . And He Who Would Be Governor,” in a special report titled “The Governors,” Washington Post, March 1, 1978, B2. ↵

- Monica Steinberg, “Uncivil Obedience: Lowell Darling Follows the Law,” American Art 34, no. 1 (Spring 2020): 112–35. ↵

- Tom Bradley to Lowell Darling, April 1, 1975, reproduced in Lowell Darling, One Hand Shaking: A California Campaign Diary (New York: Harcourt Brace Janovich, 1980), 29. ↵

- Clayton Bailey to Lowell Darling, February 1, 1977. Collection of the artist. ↵

- The performance took place on February 7, 1977. ↵

- Lowell Darling, “Urban Acupuncture,” Portland Scribe, March 24–31, 1977, 15. ↵

- National Endowment for the Arts, National Council on the Arts: Annual Report Fiscal Year 1973 (Washington, DC: National Endowment for the Arts, 1973), 103. ↵

- Darling, One Hand Shaking, 82–83. ↵

- Jeffrey W. Bullock, “A Message from the Secretary of State Jeffrey W. Bullock,” in Delaware Division of Corporations: 2021 Annual Report (Delaware Division of Corporations, 2022), 1, https://corpfiles.delaware.gov/Annual-Reports/Division-of-Corporations-2021-Annual-Report.pdf. ↵

- Paolo Woods and Gabriele Galimberti, with essay by Nicholas Shaxson, The Heavens: Annual Report (Stockport: Dewi Lewis Media, 2015). ↵

About the Author(s): Monica Steinberg is Assistant Professor in the School of Modern Languages and Cultures (American Studies) at the University of Hong Kong.